INDIAS STRENGTHENING INNOVATIVE MEDIA & ENTERTAINMENT ECOSYSTEM

FICCI FRAMES 2025, commemorate its silver jubilee, took place at the prestigious Sofitel Hotel in Mumbai on March 27, 2025. The event celebrated 25 years of fostering innovation, collaboration, and growth within the Media & Entertainment (M&E) industry.

The theme for this year’s event, “RISE Together,” encapsulates the core values of Reimagining, Innovating, Strengthening, and Empowering. FICCI FRAMES 2025 serves as a platform for industry professionals to network, exchange ideas, and collaborate on shaping the future of M&E.

The event featured insightful discussions, workshops, and presentations focused on the latest trends, innovations, and opportunities in the industry. FICCI FRAMES 2025 promises to be an influential gathering that honors the past, embraces the present, and shapes the future of the Media & Entertainment industry.

At the FICCI Frames 25 event held at Sofitel Mumbai on March 27, 2025, Ashish Shelar, Maharashtra’s Minister of Information Technology & Cultural Affairs, delivered significant insights that positioned Maharashtra as India’s emerging media and entertainment hub.

Shelar announced a groundbreaking single-window clearance system for film production permissions, representing a major shift in Maharashtra’s approach to supporting the entertainment industry.

During his address, Shelar emphasized Maharashtra’s comprehensive support for the AVGC (Animation, Visual Effects, Gaming, Comics) industry, stating that his department would implement the best suggestions from the FICCI-EY report as part of a focused 100-day program . He highlighted that Maharashtra houses the entire Bollywood ecosystem and has a rich legacy in the entertainment industry, positioning the state as the natural hub for media production.

Shelar articulated an ambitious vision positioning Maharashtra not just as India’s entertainment capital but as a global content creation hub. His policy framework demonstrates understanding of the industry’s evolving needs, particularly in the digital age where content creation extends beyond traditional Bollywood productions to include gaming, animation, and digital content.

The minister’s announcements at FICCI Frames 25 represent part of a broader 100-day implementation program designed to rapidly transform Maharashtra’s entertainment industry infrastructure . This aligns with the state’s goal to capture a larger share of India’s projected INR 3.1 trillion media and entertainment market by 2027.

Shelar’s approach emphasizes collaboration with industry bodies like FICCI, demonstrating the government’s commitment to policy-making that reflects actual industry needs rather than top-down bureaucratic decisions . His presence at the FICCI-EY report launch and active participation in industry discussions signal a new era of government-industry partnership in Maharashtra’s media sector.

The insights from Ashish Shelar at FICCI Frames 25 reveal Maharashtra’s strategic positioning to become India’s undisputed media and entertainment capital, backed by concrete policy measures, substantial financial incentives, and streamlined administrative processes that address long-standing industry pain points.

Kevin Vaz, Chairman of FICCI’s Media and Entertainment Committee and CEO – Entertainment at JioStar, delivered a powerful opening address at FICCI Frames 25 held at Sofitel Mumbai on March 27, 2025, unveiling groundbreaking insights about India’s media landscape transformation.

Vaz announced that India is on track to become the world’s third-largest media and entertainment market by 2028, driven by the unprecedented scale of content production and consumption across the country . This projection represents a significant milestone in India’s journey toward global media prominence.

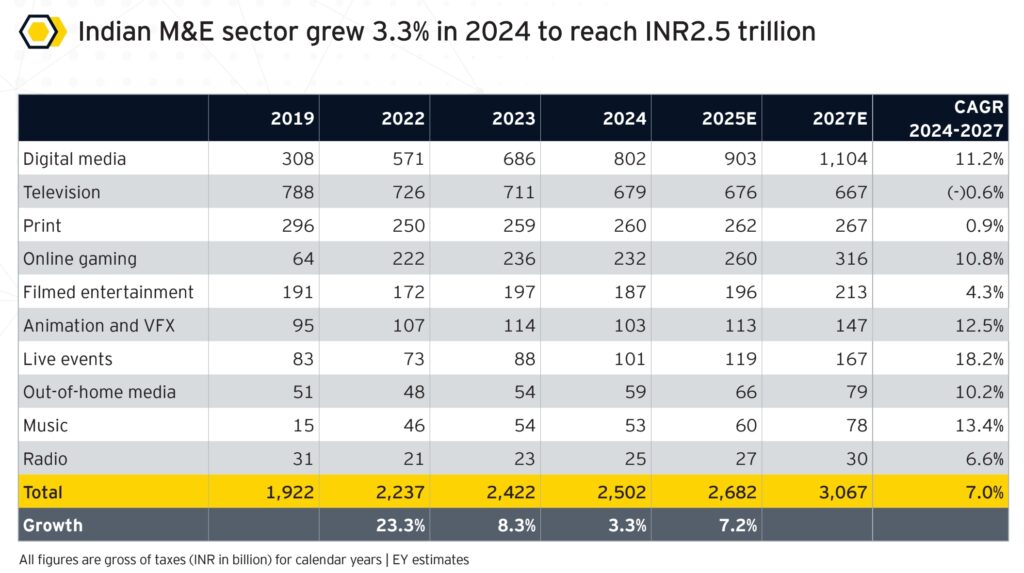

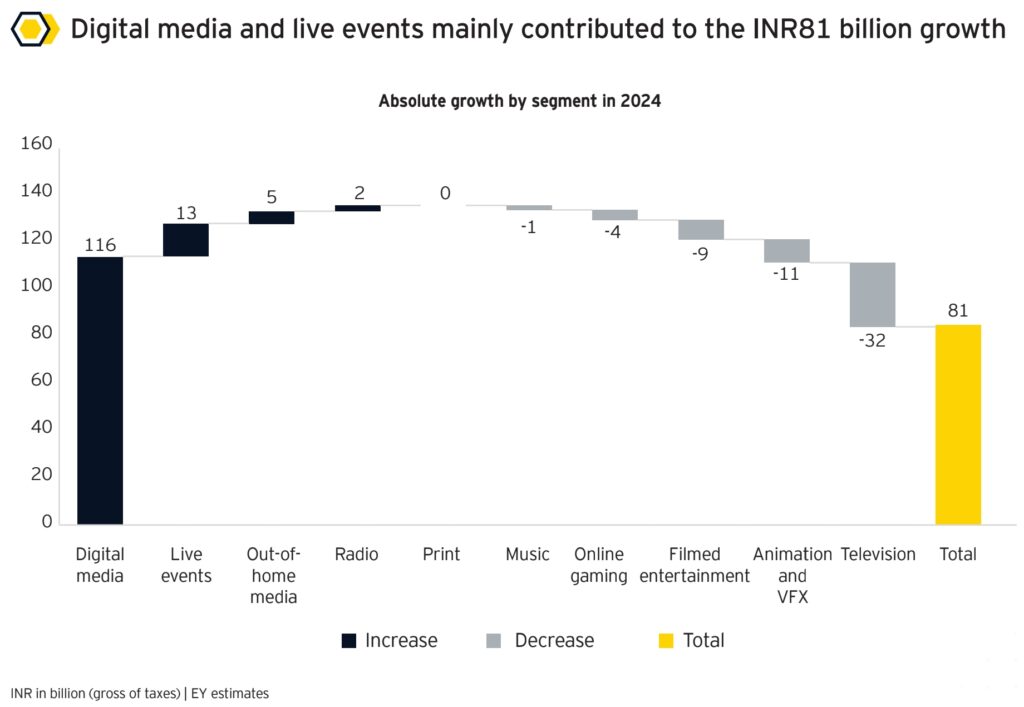

The most significant revelation from the FICCI-EY M&E Industry Report 2025 launched at the event was that digital media has overtaken television for the first time, becoming the largest segment within India’s M&E sector and contributing an unprecedented 32% to overall revenues.

This historic shift reflects India’s unique position as an “AND” market rather than an “OR” market, where television and digital media are thriving together rather than competing. Vaz emphasized this distinctive characteristic, stating that television households are projected to grow from 190 million in 2024 to 214 million by 2026, while digital platforms continue their meteoric rise.

Vaz highlighted the powerful role of sports, particularly the Indian Premier League (IPL), in demonstrating the synergy between traditional and digital platforms. IPL 2024 reached 525 million viewers on TV and 550-600 million on streaming platforms, showcasing the immense potential of India’s dual-screen ecosystem.

The address celebrated Southern cinema’s exceptional success in bringing Indian storytelling to global audiences, with films like RRR, KGF-2, and Kantara captivating viewers worldwide and collectively grossing hundreds of crores . Vaz noted that 2024 was a landmark year for pan-India cinema, with successes like Pushpa 2 achieving unprecedented cross-regional appeal.

Despite digital media’s dominance, Vaz emphasized that television remains the bedrock of the industry, commanding over 30% of the market . He dismissed Western trends suggesting television’s decline among younger audiences, noting that in India, television continues to be affordable, accessible, and deeply ingrained in households.

Vaz celebrated India’s growing international influence, highlighting achievements “from global recognition at Cannes and the Oscars to our rise as a VFX powerhouse” . He specifically mentioned India’s involvement in creating VFX masterpieces like the Oscar-nominated Emilia Pérez and Mufasa: The Lion King.

Looking ahead, Vaz expressed confidence that OTT platforms are set to become a major force in digital entertainment while television maintains its foundational role. He emphasized that India’s media ecosystem embraces “innovation without abandoning tradition”, creating unique opportunities for growth and creativity.

The insights revealed at FICCI Frames 25 demonstrate India’s media and entertainment industry’s remarkable resilience, innovation, and global potential, with Kevin Vaz positioning the sector for unprecedented growth toward becoming a dominant force in the worldwide media landscape by 2028.

Ashish Pherwani, Partner and Media & Entertainment Leader at EY India, delivered profound insights during the launch of the FICCI-EY Media and Entertainment Industry Report and BAF Awards 2025 at Sofitel Mumbai on March 27, 2025. His most significant observation was the achievement of India’s “digital inflection point” – a milestone that EY had predicted would occur by 2023 but actually materialized in 2024.

“Finally, the digital inflection point. And it changes everything,” Pherwani declared, marking the historic moment when digital media surpassed television as the largest segment of India’s media and entertainment industry for the first time in 25 years.

Pherwani introduced a groundbreaking analytical framework explaining how digital media has fundamentally redefined the M&E sector’s value proposition. He articulated that media and entertainment companies now provide consumer value across four critical tenets:

1. Information” Information to live life better, through news and communities” – Media serves as a vital source of knowledge that helps consumers make better life decisions.

2. Escapism” Escapism to forget troubles by getting immersed in fiction and reality content” – Traditional entertainment value where consumers seek relief from daily stresses through engaging content.

3. Materialism” Materialism to enable commerce through funded content and e-commerce” – The integration of commerce and content, enabling direct purchasing and commercial transactions through media platforms.

4. Self-Actualization” Self-actualization via social media, professional portals and the creator economy” – Platforms that enable personal growth, professional development, and creative expression.

“Every media and content company is now evaluated by consumers against the utility it provides across the above tenets,” Pherwani emphasized, explaining how this framework “is driving how traditional and new media companies are redefining their product, processes, customer acquisition and purpose”

The EY leader outlined India’s M&E sector growth from INR 2.5 trillion in 2024 with projections to reach INR 2.7 trillion in 2025 (7.2% growth) and INR 3.1 trillion by 2027.

Pherwani revealed that digital media grew by 17% to reach INR 802 billion, crossing the INR 80,000 crore threshold and becoming the largest segment by contributing 32% of total M&E revenues in 2024 . He projected that digital media will be the first segment to overcome the INR 1 lakh crore threshold in advertisement revenue by 2026.

Pherwani provided nuanced insights into sector performance, noting “a very big mixed bag” where:Four segments experienced strong growth: Digital (17%), events (15%), OOH media, and radio Five segments experienced decline: Traditional TV subscription, print subscription, films, music, and animation/VFX Advertising grew 8%, but subscription revenues fell 2%.

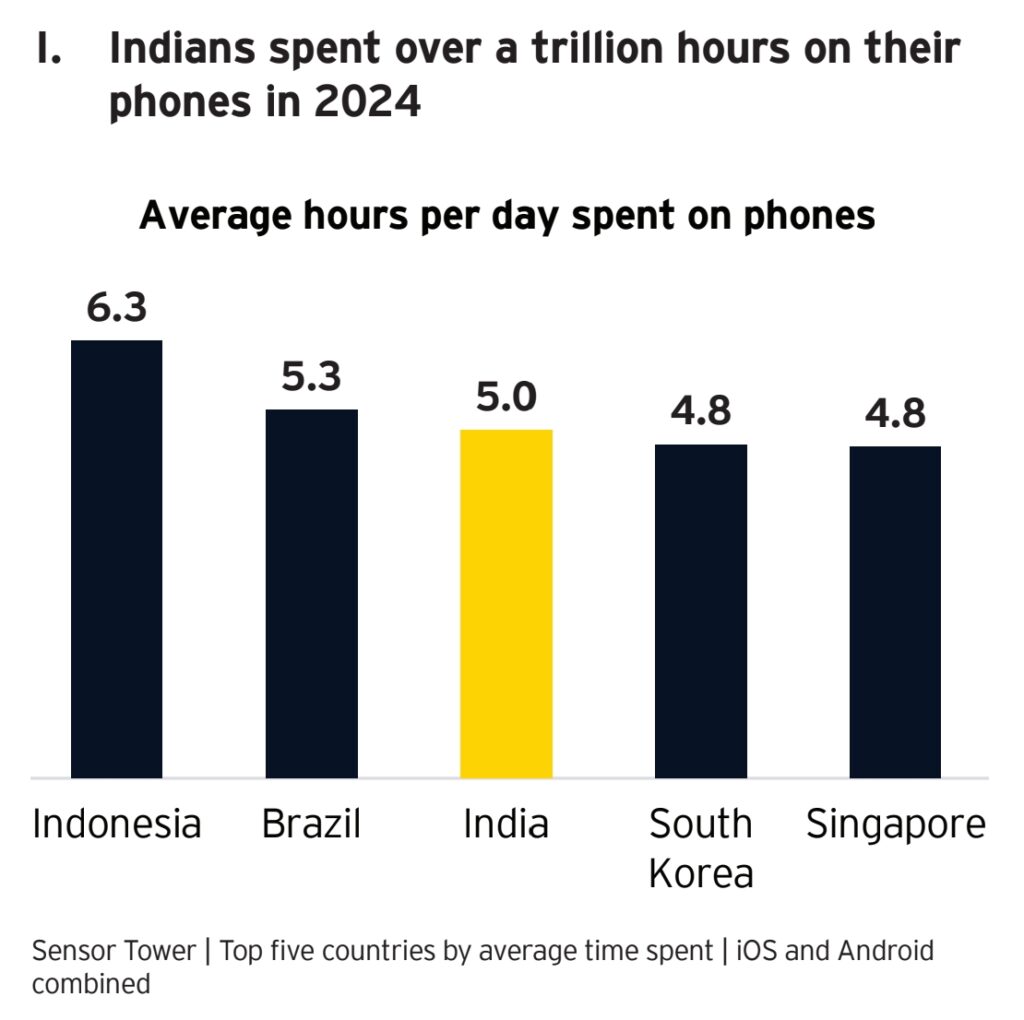

Pherwani’s analysis revealed that Indians spend an average of 5 hours daily on smartphones, with nearly 70% of this time dedicated to social media engagement, gaming, and video streaming . This behavioral shift supports the digital inflection point thesis and explains the fundamental transformation in media consumption patterns.

Arjun Nohwar, Co-Chair of the FICCI Media and Entertainment Committee and Senior Vice President & Country General Manager for India & South Asia at Warner Bros. Discovery, delivered transformative insights at FICCI Frames event in Bombay. He presented a comprehensive vision for India’s media and entertainment future.

Nohwar’s most profound insight centered on a paradigm shift: “We are no longer in the content business; we are in the experience business.” This transformation reflects how modern audiences have evolved from passive consumers to active participants in immersive entertainment ecosystems.

Nohwar emphasized that the real challenge has evolved: “The real battle is not just for viewership, but engagement.” He explained that modern audiences multitask across screens while consuming content, creating a complex engagement ecosystem where:

Viewers are scrolling, shopping, commenting, and engaging in real-time

Television now competes with second and third screens, not just other networks

Attention spans are fleeting, but expectations are higher than ever

Nohwar highlighted that 2024 marked a historic shift where digital media overtook television to become the largest M&E segment, contributing 32% to overall revenues—the first time in 20 years that television was not the dominant segment.

Four Pillars of Future GrowthLinear Television’s Reinvention:

Traditional TV evolving through connected ecosystems and bundled experiences

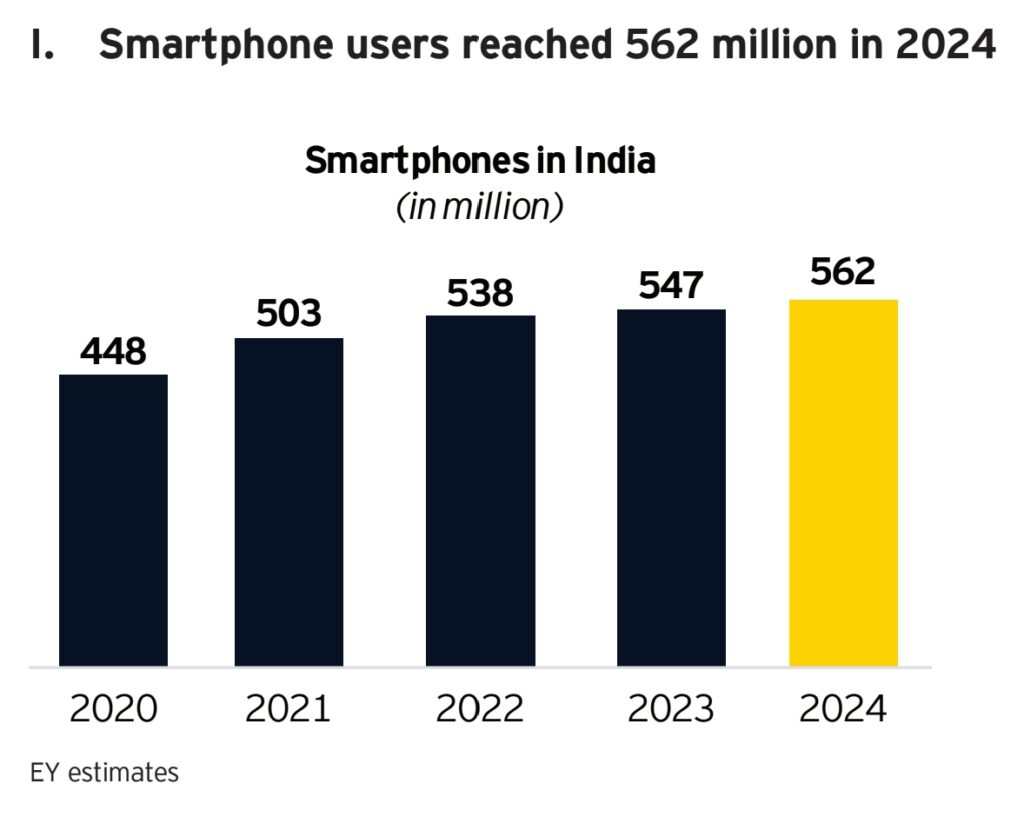

OTT Expansion: With over 550 million users, driven by regional content and AI-powered personalization

SME Advertising & Performance Marketing: Reshaping content consumption patterns

India as Global Storytelling Hub: Transitioning from content consumer to global storytelling epicenter

“Indian stories are no longer confined by geography, language, or platform. We are creating stories and content that not only resonate across diverse audiences but are also capturing global imagination,” Arjun said.

Nohwar emphasized Warner Bros. Discovery’s commitment through strategic investments in technology hubs in Bangalore, Hyderabad, and Pune, advancing AI capabilities and global video advertising innovations. He stressed the importance of “blending traditional studios, digital platforms, independent creators, and technology enablers” to spawn new storytelling models.

Nohwar acknowledged the seismic shift in India’s entertainment landscape: “Bollywood, which once held a dominant 44% share of the Indian box office, has now conceded its leadership position to southern cinema, which accounts for nearly 50% of the market.”

With OTT platforms reaching 111 million subscriptions across 47 million households, Nohwar identified subscription fatigue as a significant challenge. He highlighted new bundling models integrating streaming, gaming, and commerce as solutions for creating seamless entertainment ecosystems.

Nohwar quoted: “India’s time is now. Let’s make the world listen. Let’s make the world watch.” He emphasized that the question is no longer whether India will lead in M&E, but “how boldly we choose to define that leadership.”

The FICCI Frames 2025 “Future of Pay TV” panel discussion took place on March 27, 2025, at Hotel Sofitel BKC, Mumbai, not on March 25 as initially queried. This was part of the FICCI-EY Media & Entertainment Report Release and BAF Awards 2025 event, which celebrated FICCI Frames’ silver jubilee milestone.

Major Insights from the Panel DiscussionPay TV’s Resilience in IndiaThe panel explored why Pay TV is still thriving in India, driven by several key factors:

Cultural consumption habits deeply rooted in Indian households

Strong regional channel preferences that maintain viewer loyalty

Family-oriented consumption patterns where television remains central to household entertainment

Affordability factor with India maintaining among the world’s lowest television costs at $2.50-$3.50

The discussion occurred against the backdrop of a historic digital inflection point, where digital media overtook television as the largest M&E segment for the first time, contributing 32% of total revenues in 2024. However, the panel emphasized that India operates as an “AND” market rather than an “OR” market, where television and digital platforms thrive together rather than compete.

The panelists discussed the evolution toward four equitable modes of TV distribution:

Traditional Cable/DTH

Free-to-Air Television

Connected TV/Smart TV

Direct-to-Mobile (D2M) services

The panel highlighted Connected TV’s massive growth, expanding from 30 million to significant penetration, though ARPU remains challenging at current pricing levels.

The discussion addressed serious concerns, including findings from AIDCF’s survey of 28,000 local cable operators, which revealed that 35% experienced a 40% decline in their subscriber base since the pre-COVID period. This highlighted the urgent need for industry collaboration to ensure Pay TV’s survival.

The panel emphasized the importance of AI and technological advancement in transforming the sector. Dwivedi described AI as “not an elephant but a dragon” that could either be tamed as an ally or emerge as a formidable force, requiring industry evolution in perspective

Despite current challenges, the television sector is projected to grow from 190 million households in 2024 to 214 million by 2026. The overall M&E sector is expected to achieve 7.2% growth in 2025, reaching ₹2.7 trillion, with further expansion to ₹3.1 trillion by 2027.

The panel discussed the necessity for multi-format content creation to serve different audience segments, particularly younger demographics who consume news and entertainment across social and digital platforms.

Industry experts highlighted expectations for innovative pricing models and windowing strategies for media companies to leverage all distribution platforms effectively. The discussion emphasized bundling opportunities with telecom packages and multi-platform combinations.

The “Future of Pay TV” panel positioned India’s television industry within the broader context of becoming the world’s third-largest media and entertainment market by 2028. The discussion emphasized that while digital transformation accelerates, television remains the bedrock of India’s media ecosystem, commanding over 30% of the market and maintaining its role as an affordable, accessible medium deeply ingrained in Indian households.

The event successfully demonstrated that rather than facing obsolescence, Pay TV in India is evolving through technological integration, strategic partnerships, and innovative distribution models while maintaining its cultural relevance and expanding its reach through connected platforms.

The “Shape of the Future: Print” fireside chat session was moderated by Ashish Pherwani, Partner at EY, and featured two industry titans: Girish Agarwal (Promoter Director, Dainik Bhaskar Group) and Sivakumar Sundaram (CEO – Publishing, Bennett Coleman & Co. Ltd. – Times of India Group).

The most striking revelation from the panel was that Indian newspapers operate at a remarkable 28% EBIT margin, significantly outperforming many digital businesses that struggle to achieve profitability. Girish Agarwal emphasized this competitive advantage, stating that “many digital businesses struggle to define profitability” while newspapers maintain robust financial performance.

Agarwal dispelled misconceptions about print decline by revealing that Dainik Bhaskar “made a record profit in 2023-24 since our listing”, demonstrating the continued financial viability of well-managed print operations.

Ashish Pherwani opened the discussion by acknowledging the resilience of print media, noting that “Even in this tough year, print has grown. That is such a heartening story for the world, and I believe the world should learn from India”. This growth occurred despite widespread digital disruption across global markets.

Girish Agarwal attributed print’s sustained success to its “strong foundation and fundamental business model”. He explained that newspapers possess a unique “right of way” into people’s homes and daily routines, creating long-term bonds with consumers that digital platforms struggle to replicate.

Sivakumar Sundaram highlighted a crucial differentiator: “In the digital world, we are trapped in echo chambers, seeing only what aligns with our beliefs. Newspapers provide an opportunity to discover new perspectives, breaking away from digital algorithms”. This positions print as essential for diverse information consumption.

The panel emphasized print’s continued investment in quality journalism. Agarwal revealed that Dainik Bhaskar employs “7,000 journalists across the country, covering diverse and often difficult stories. They go to great lengths, even risking their lives, to uncover the truth”. This ground-level reporting capability represents a competitive advantage over digital-only platforms.

Sundaram demonstrated print’s resilience by stating: “Even during COVID, when we were down to 10%, we continued investing in print. Today, as digital screens get smaller, the demand for real, tactile experiences grows, reinforcing the importance of newspapers”.

Agarwal emphasized that print media will “continue to adapt, especially in tier 2 and beyond cities, where people still have the time to engage deeply with newspapers”. This aligns with India’s demographic and economic expansion beyond metropolitan areas.

Sundaram stressed newspapers’ crucial role in “keeping not just readers but also the government and judiciary informed, ensuring a thriving democracy”. This positions print as essential infrastructure for democratic governance rather than merely commercial enterprise.

Agarwal raised concerns about digital platforms relying on newspapers for content without maintaining their own reporting capabilities: “Google approaches newspapers for content because they know they don’t have teams to gather news. Some publications make the mistake of giving their content away instead of driving readers directly to their platforms”.

The panelists expressed confidence in print’s adaptability. Agarwal stated: “If the format ever changes, we will evolve with it”, indicating willingness to innovate while maintaining core print strengths.

Sundaram emphasized “resilience and relevance” as key content strategy elements, while Agarwal encouraged the industry to “stay honest to our profession” and continue successful practices from 2024 into 2025 and beyond.

According to the FICCI-EY Report 2025, the print segment is projected to grow to ₹267 billion by 2027, despite digital media becoming the largest M&E segment for the first time in 2024. Print advertising revenues grew 4% in 2023, with circulation growing 3%.

The panel occurred within the context of Hindi and regional language publications recovering to around 93% of pre-COVID levels, while English publications recovered to 74%. This demonstrates the particular strength of vernacular print media in India’s market.

The “Shape of the Future: Print” discussion positioned newspapers not as declining legacy media, but as essential democratic infrastructure with unique advantages in credibility, deep engagement, and local market penetration. The panel demonstrated that rather than competing directly with digital platforms, successful print operations are leveraging their inherent strengths—tactile experience, editorial credibility, and intimate community connections—to maintain relevance and profitability in India’s evolving media landscape.

The session concluded with optimism about print’s role in India’s media ecosystem, emphasizing that successful adaptation and honest journalism will continue driving growth, particularly in India’s expanding tier-2 and tier-3 markets where newspaper reading remains deeply integrated into daily routines.